How to Calculate Effective Credit Card Processing Rate: A 2026 Merchant Audit Checklist

What if the "low rate" promised on your monthly statement is actually a carefully disguised math problem designed to hide your true costs? Most business owners feel a sense of dread when they open their merchant reports, facing a wall of non-standardized jargon and unexplained fee hikes. You deserve to know exactly where your hard-earned money is going. Learning how to calculate effective credit card processing rate is the only way to cut through the noise and find the single truth of your business's financial health.

We understand that you've likely spent hours trying to distinguish between mandatory bank fees and the markups your processor adds on top. This article promises to help you master the math behind your statement so you can uncover hidden junk fees and protect your bottom line. We'll provide a step-by-step 2026 audit checklist that identifies negotiable charges and shows you how to arrive at a single, honest percentage for your total costs. By the end of this guide, you'll have the tools to improve your cash flow and act as your own best advocate in the complex world of merchant services.

Key Takeaways

- Use the effective rate as a universal metric to clearly compare different pricing models like flat-rate or interchange-plus.

- Learn how to calculate effective credit card processing rate by dividing your total monthly fees by your gross sales volume.

- Identify "junk fees" such as PCI compliance or portal charges that often hide behind confusing industry terminology on your statement.

- Cross-reference your merchant statement totals against your point of sale reports to ensure every dollar is accounted for correctly.

- Streamline your cash flow by removing unnecessary markups and choosing processing partners who prioritize transparent reporting.

What is an Effective Credit Card Processing Rate?

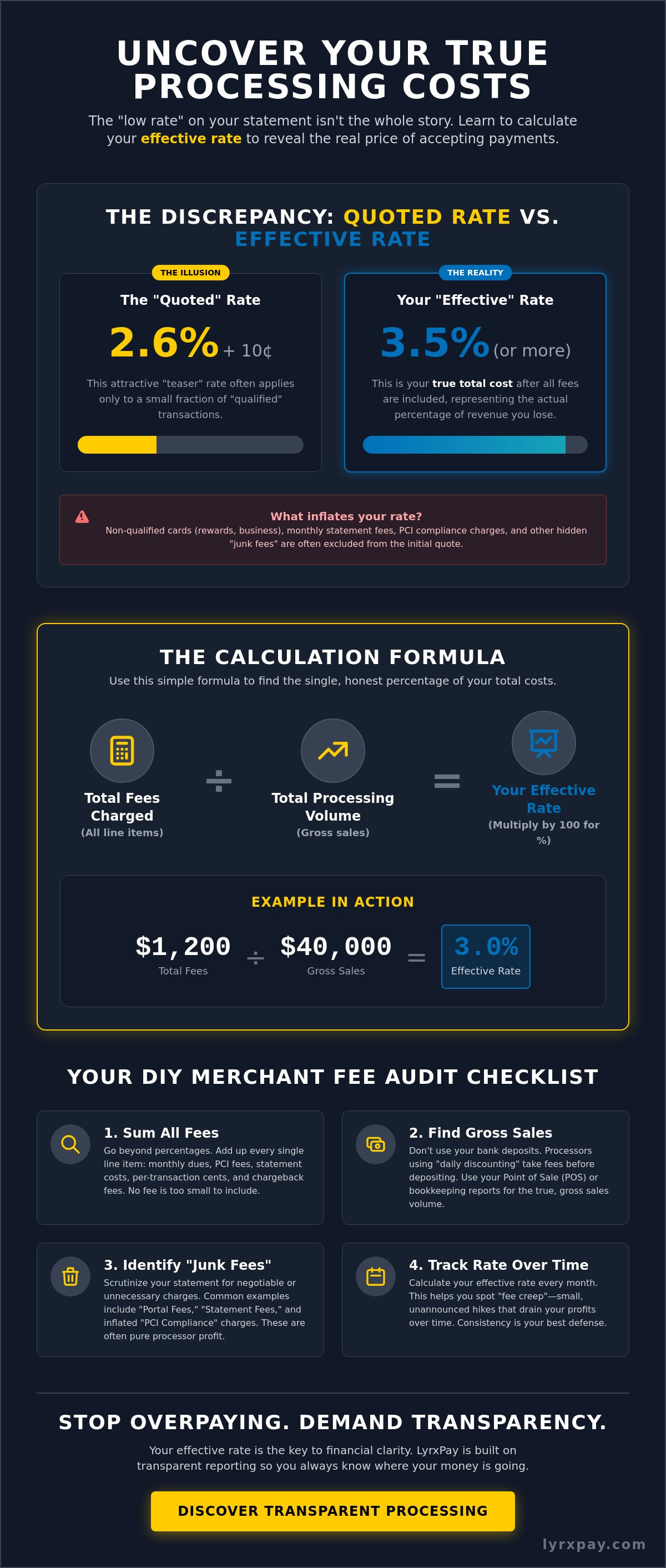

Think of your effective rate as the "bottom line" of your merchant services. While a salesperson might lead with a flashy percentage for a single transaction type, that number rarely tells the whole story. Your effective rate represents the actual, total percentage of revenue lost to fees once everything is tallied at the end of the month. It is the great equalizer. Whether you're on a flat-rate plan, tiered pricing, or interchange-plus, this single figure allows you to compare different providers apples-to-apples. Understanding how to calculate effective credit card processing rate is the first step toward financial transparency and protecting your business's liquidity.

Many business owners find that their actual costs are significantly higher than what they were promised during the initial pitch. This happens because merchant statements are often intentionally complex. By focusing on the effective rate, you bypass the marketing jargon and see the reality of your cash flow. If your total fees consume 3.5% of your gross sales, it doesn't matter if you were promised a "2.6% rate." The 3.5% is your reality. Monitoring this metric ensures that you aren't overpaying for the simple act of accepting payments.

THE DISCREPANCY BETWEEN QUOTED AND ACTUAL COSTS

Teaser rates are a common tactic in the industry. A processor might quote you a low percentage that only applies to "qualified" transactions, such as basic debit cards. However, when customers use premium rewards cards or business credit cards, those transactions often fall into "non-qualified" tiers with much higher costs. These surcharges, combined with the foundational interchange fee set by card networks, can quickly inflate your expenses. Monthly fixed costs, such as statement fees or PCI compliance charges, also push your total percentage higher. For example, a business with a 2.9% flat rate and a small average ticket size might actually see a 3.6% effective rate once per-transaction cents and monthly fees are included.

WHY THIS METRIC IS YOUR BEST DEFENSE

Reliable data is your strongest tool in any negotiation. When you learn how to calculate effective credit card processing rate, you gain the power to spot "fee creep" before it drains your bank account. Processors sometimes implement small, unannounced hikes that are easy to miss if you only look at individual line items. By tracking your effective rate over several months, you can identify these trends and demand an explanation. This clarity also helps you set more accurate prices for your products. If you know exactly what it costs to process a dollar, you can ensure your margins remain healthy and your business stays resilient.

The Step-by-Step Calculation Formula

Ready to strip away the complexity? Finding your true cost is a straightforward process once you know which numbers to pull from your month-end statement. You won't find this "effective rate" listed in a bold font on your bill because many providers prefer it remains a mystery. Learning how to calculate effective credit card processing rate requires you to act as your own auditor. By gathering raw data, you reveal the single percentage that actually impacts your liquidity. This transparency is the foundation of a healthy financial partnership.

To perform your own audit, follow these simple steps:

- Locate your Total Processing Volume (the gross amount of sales before any fees were deducted).

- Identify the Total Fees Charged (the sum of all percentage fees, per-transaction cents, and monthly dues).

- Divide the Total Fees by the Total Volume.

- Multiply that result by 100 to find your percentage.

THE EFFECTIVE RATE FORMULA IN ACTION

If your business processed $40,000 in sales and your total fees were $1,200, the math is $1,200 / $40,000 = 0.03, or a 3.0% rate. You must include every line item in that numerator to get an honest result. This covers PCI fees, statement costs, and per-transaction cents. As noted in this guide on Credit Card Processing Fees, these secondary costs often go unnoticed. Include chargeback fees in your total, but keep the lost sale amount separate to avoid skewing the percentage.

ACCOUNTING FOR GROSS VS. NET SETTLEMENT

Accuracy is difficult if your processor uses "daily discounting." In this scenario, they take fees before the money ever hits your bank account. If you only look at deposits, your volume appears lower than reality, which makes your rate look higher. You should use your POS reports or integrated bookkeeping software to find your true gross sales. Cross-referencing these reports ensures your audit is based on actual revenue. For growing businesses, next-day deposits make this reconciliation much faster and keep your cash flow predictable.

Consistency is your best indicator of a fair deal. If your rate jumps by more than a few basis points without a significant change in your sales volume, it is time to ask your processor for a detailed explanation.

Analyzing the 'Fat' in Your Statement

Once you've mastered how to calculate effective credit card processing rate, the next step is performing a forensic audit of where that money actually goes. Not every fee is negotiable. To protect your resources, you must separate the "wholesale" costs from the "markup" added by your provider. Think of your statement as a grocery bill where some items are fixed commodities and others are premium service charges. Identifying the "fat" in these reports allows you to trim unnecessary expenses and keep more of your revenue.

Your total cost is primarily built on three pillars: interchange, assessments, and the processor’s margin. A significant portion of your bill goes toward understanding credit card processing fees at the network level. Visa and Mastercard set these foundational rates, which vary based on your Merchant Category Code (MCC). If you are categorized as high-risk, your baseline costs will naturally be higher. However, many processors hide their own profits inside these complex categories, making it difficult to see where the bank's fee ends and the processor's profit begins.

The 2026 landscape adds a new layer of complexity with the rise of digital wallets and blended ACH rates. While Apple Pay and Google Pay use the same rails as traditional cards, their security protocols can sometimes influence your rate. The way your business accepts payments also matters. In-person transactions generally range from 1.8% to 2.6%, while online or keyed-in transactions jump to between 2.25% and 3.5%. If your business has shifted toward more digital sales, your effective rate will naturally climb. This context helps you determine if a rate hike is due to your sales mix or a hidden fee increase.

WHOLESALE COSTS: INTERCHANGE AND ASSESSMENTS

Interchange fees are the non-negotiable heart of processing. These are paid to the card-issuing bank and typically range from 1.15% to 3.15% as of mid-2026. On top of this, you pay assessment fees directly to the card brands, usually around 0.13% to 0.15%. Your specific "payment mix" dictates these costs. If your customers favor high-end rewards cards, your effective rate will be higher than a business that primarily processes debit cards at 0.5% to 1.5%. You cannot change these wholesale prices, but you can certainly change who manages them for you.

PROCESSOR MARKUP: WHERE YOU CAN SAVE

The processor markup is where you find the most room for negotiation. This is the "fat" you want to trim. Look for line items like statement fees, portal fees, or annual PCI compliance charges. These are often "junk fees" that provide little value to your operations. If you see "Non-Qualified" surcharges, you are likely on a tiered pricing model that is costing you significantly more than an interchange-plus model. Knowing how to calculate effective credit card processing rate gives you the leverage needed to challenge these markups. Focus on the basis points added on top of wholesale costs. A fair markup should be transparent and consistent.

Checklist: Performing a DIY Merchant Fee Audit

Having the formula is only half the battle. To truly understand how to calculate effective credit card processing rate, you must know exactly where to find the numbers on a statement designed to be confusing. Most reports hide the "Total Volume" and "Total Fees" on different pages, often buried under headers like "Processing Summary" or "Activity Detail." Start your audit by pulling your most recent month-end report and opening your point of sale software. Consistency between these two sources is the first sign of a healthy merchant account.

Follow this checklist to perform a forensic review of your costs:

- Cross-check Total Volume: Match the "Gross Sales" on your statement with your POS "Sales by Payment Type" report. If they don't align, you may be paying fees on "ghost" transactions or uncaptured authorizations.

- Flag the Jargon: Highlight any line item containing the words "Surcharge," "Non-Qual," or "Misc Fee." These are almost always processor markups that can be negotiated or removed.

- Verify PCI Compliance: Check if you are being charged a monthly "PCI Fee" on top of an annual "Compliance Fee." You should never be double-charged for security standards.

- Benchmark Your Results: In 2026, average fees range from 1.5% to 3.5%. If your effective rate for in-person sales is climbing toward 3.0%, you are likely overpaying for basic processing.

- Separate ACH Rails: Calculate your ACH costs in a separate bucket. Since ACH fees are significantly lower than credit card rates, blending them into one figure hides the true cost of your card transactions.

THE RED FLAG LIST

Some fees exist simply to drain your liquidity. Look closely for "Batch Header" fees charged every single day. While a small fee is standard, some providers inflate this cost to create a steady stream of passive revenue. Inactivity fees or "minimum processing" penalties are also common red flags. If your business has a slow month, you shouldn't be punished with an extra surcharge. Finally, watch for hidden markups on corporate or international cards. These often appear as "Interchange Differential" and can add significant weight to your total percentage.

OPTIMIZING YOUR PAYMENT MIX

Your sales method dictates your baseline. Analyzing the percentage of transactions coming through high-cost digital wallets helps you understand why your rate fluctuates. If you handle B2B transactions or high-ticket invoices, you should ask if your processor supports Level 2 or Level 3 data processing. This technical step provides more information to the card networks, which can lower your wholesale costs on corporate cards. If your current provider can't offer this transparency, it's time to switch to a partner that prioritizes your bottom line. Encouraging ACH for larger invoices is another simple way to protect your margins without changing your pricing.

Stop Overpaying: LyrxPay’s Transparent Approach

You've done the math. You now know how to calculate effective credit card processing rate and have identified the "fat" in your monthly statement. But knowledge is only the first step. The real challenge is finding a partner who values your bottom line as much as you do. We believe in total transparency. Our team acts as a defender of your resources, ensuring you never face another sudden fee hike without a clear explanation. By moving away from confusing tiered models, we help you regain control over your business's financial health.

Efficiency shouldn't stop at the transaction. Many merchants struggle with the ripple effect that high processing costs and complex reporting have on their accounting. If your fees are deducted before deposits hit your bank, your bookkeeping becomes a nightmare. We solve this by offering seamless QuickBooks and Xero integrations that eliminate manual data entry. This "concierge" level of service extends to our bookkeeping and payroll solutions, creating a unified ecosystem where your data flows accurately from the point of sale to your final financial reports.

THE LYRXPAY ADVANTAGE: CLARITY AND SPEED

We prioritize interchange-plus pricing because it's the most honest way to do business. This model separates the wholesale cost from our small, fixed markup, making it easy to see exactly what you're paying for. Combined with our modern point of sale software and hardware, this approach reduces reconciliation errors and improves your overall liquidity. Next-day deposits mean your money is available when you need it, not sitting in a processor's holding account. We've already done the heavy lifting so you can focus on your craft.

NEXT STEPS FOR A HEALTHIER BOTTOM LINE

Reclaiming your margins starts with a single conversation. If you're still unsure how to calculate effective credit card processing rate for your specific industry, our Texas-based team is ready to help. We offer a clear path forward through a free, no-obligation statement audit. We'll look at your current numbers, flag the junk fees, and show you exactly how much you could save by switching to a more integrated payroll and bookkeeping system. Get a free rate review today and experience the relief of a partnership built on integrity and results.

PROTECT YOUR PROFIT MARGINS

Taking control of your merchant services shouldn't feel like a second job. You now have the audit checklist to strip away the mystery and the formula to find the truth behind the marketing jargon. By identifying hidden junk fees and understanding your specific payment mix, you've moved from a state of curiosity to a state of confidence. Mastering how to calculate effective credit card processing rate is the ultimate tool for protecting your liquidity and ensuring your pricing remains competitive in a shifting 2026 market.

You don't have to handle the heavy lifting of financial management alone. Our Texas-based team is ready to act as your professional concierge, providing the next-day deposits you need for better cash flow and expert QuickBooks or Xero integration to simplify your bookkeeping. We believe in advocacy over transactions and transparency over complexity. Stop overpaying—get your free merchant statement audit from LyrxPay and start keeping more of what you earn. You've worked hard to build your business. It's time your processor worked just as hard to protect your success.

Frequently Asked Questions

What is a good effective credit card processing rate in 2026?

A competitive effective rate in 2026 typically sits between 2.0% and 3.5% for most retail and service businesses. If your sales are primarily in-person, you should aim for the lower end of that range. Online businesses naturally see higher rates due to increased security risks. Tracking this number monthly helps you ensure your processor isn't quietly inflating their markup over time.

Can I negotiate my merchant processing fees down?

You can absolutely negotiate the markup portion of your fees. While the interchange rates set by card brands are non-negotiable, the basis points and monthly service fees added by your processor are flexible. Presenting your provider with a clear breakdown of how to calculate effective credit card processing rate shows them you are an informed partner. This leverage often leads to the removal of unnecessary junk fees.

Is a flat-rate processor like Square or Stripe cheaper than a merchant account?

Flat-rate processors are often more expensive for businesses processing over $10,000 per month. While the simplicity of a single rate is appealing, you often pay a premium for that convenience. Merchant accounts using interchange-plus pricing allow you to keep the savings when customers use low-cost debit cards. For growing companies, the transparent "pass-through" model almost always results in a lower total cost.

How do I find hidden fees on my merchant statement?

Hidden fees often hide behind ambiguous labels like "Administrative Supplement" or "Regulatory Mandate." Start by scanning the "Other Fees" section of your statement for any recurring monthly charges that weren't in your initial contract. Cross-referencing these with your actual sales volume will reveal if these costs are scaling unfairly. If a fee doesn't provide a clear service, it is likely a candidate for removal.

Why does my effective rate change every month?

Your rate fluctuates based on what your customers put in their wallets. If more customers use high-end rewards cards or corporate cards in a specific month, your wholesale costs will rise. Changes in your average transaction size also play a role since per-transaction cents have a larger impact on smaller sales. Understanding these shifts helps you distinguish between natural market changes and processor-led fee hikes.

Does QuickBooks integration affect my processing rates?

Integrated QuickBooks and Xero solutions don't directly change your interchange rates, but they drastically lower your "internal" effective rate. By eliminating manual data entry and reconciliation errors, you save hours of administrative labor every month. This efficiency allows you to focus on growth rather than chasing down missing transaction data. A partner who offers these integrations is invested in your total operational health.

What are 'non-qualified' fees and how do I avoid them?

Non-qualified fees are surcharges triggered when a transaction fails to meet the "qualified" criteria of a tiered pricing plan. This often happens with rewards cards, international cards, or keyed-in entries. You can avoid these traps by switching to an interchange-plus model. This ensures you pay the true cost of every card without arbitrary penalties that inflate your monthly expenses.

How often should I audit my merchant statement?

You should perform a brief audit every single month when your statement arrives. This proactive habit allows you to catch "fee creep" before it drains significant revenue from your bank account. If you notice a steady climb in your costs, it is time to use our guide on how to calculate effective credit card processing rate to verify the math. Regular reviews keep your processor honest and your cash flow predictable.