How to Lower Merchant Fees: The 2026 Strategic Guide for Business Owners

What if the complex "junk fees" cluttering your monthly statement were actually a hidden roadmap to recapturing thousands in lost revenue? You've likely felt that familiar sting of frustration while staring at a merchant statement that looks more like a riddle than a financial document. It's exhausting to watch your hard-earned margins get chipped away while you search for how to lower merchant fees without disrupting your daily operations. You deserve a partner who defends your resources rather than draining them.

You don't have to accept these rising costs as an inevitable price of doing business. This strategic guide reveals the exact steps to audit your statements for hidden markups, leverage the 10-basis-point reductions from the 2026 interchange settlement, and implement high-efficiency routing. If you apply these managed care principles to your processing, you can transform your financial operations from a source of stress into a streamlined engine for growth.

We'll walk through the process of eliminating unnecessary costs, securing next-day deposits to boost your liquidity, and ensuring every transaction syncs perfectly with QuickBooks for total office harmony.

Key Takeaways

- Master the "Effective Rate" calculation to cut through statement complexity and reveal the true cost of your processing.

- Discover how to lower merchant fees by leveraging Level 2 and Level 3 data for B2B transactions and using ACH for high-value invoices.

- Implement immediate operational wins by prioritizing card-present hardware over keyed entries to secure the lowest possible interchange rates.

- Adopt a "Managed Care" approach by integrating your payment processing with QuickBooks and payroll to eliminate administrative friction and protect your margins.

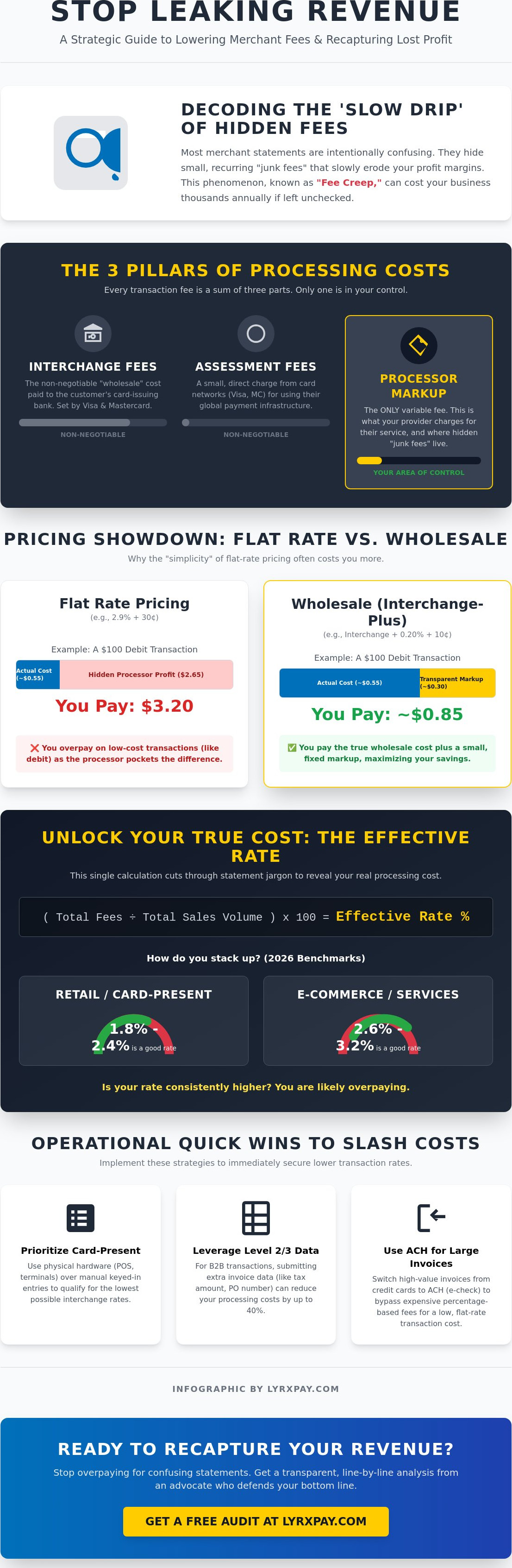

Decoding the 'Slow Drip': Why Your Merchant Fees Keep Rising

Most business owners don't realize their profit margins are being eroded by a phenomenon known as "Fee Creep." It isn't a sudden, massive price hike that triggers an alarm. Instead, it's a slow, quiet addition of small surcharges and unannounced rate adjustments that appear over several months. You shouldn't have to be a forensic accountant to understand your monthly bill. If your statements feel like a riddle, it's likely because the industry's complexity is being used as a shield to hide rising costs. Understanding how to lower merchant fees begins with a clear-eyed look at what makes up your total cost of acceptance.

Think of your merchant fees as a cumulative total of three distinct layers. While some of these costs are set in stone by the global card networks, others are entirely within your power to change. We view ourselves as a defender of your resources. Our goal is to help you distinguish between the "wholesale" costs of the financial world and the unnecessary markups that some providers quietly layer on top of your transactions. When you can see the difference, you gain the leverage needed to protect your bottom line.

The Three Pillars of Processing Costs

To gain control over your expenses, you must understand the three specific components of every transaction:

- Interchange Fees: These are the non-negotiable rates set by card brands like Visa and Mastercard. They represent the "wholesale" cost of the transaction and are paid to the bank that issued the customer's card.

- Assessment Fees: These are direct charges from the card networks for using their global infrastructure. Like interchange, these are generally unavoidable for any business accepting cards.

- Processor Markup: This is the only area where you have significant leverage. This is the fee your provider charges for their services, and it is often where "junk fees" are hidden.

Why 'Flat Rate' Pricing Often Costs You More

Many providers offer a flat rate, such as 2.9% plus a fixed cent amount, because it feels simple. However, this simplicity often comes with a "convenience tax" that can be incredibly expensive. Flat-rate pricing hides the true cost of transactions that have very low interchange rates, such as regulated debit cards. In these cases, the processor pockets the massive spread between the actual cost and the flat rate you're paying.

If you want to maximize your savings, it's time to move toward a more transparent model. Transitioning to wholesale credit card processing rates is the gold standard for transparency. This approach ensures you pay the exact interchange cost plus a small, fixed markup, allowing you to benefit from lower-cost transactions rather than letting your processor keep the difference. Learning how to lower merchant fees effectively means demanding this level of clarity in every statement you receive.

The Merchant Statement Audit: How to Identify Overcharges

You shouldn't have to spend your weekend playing detective just to understand where your money is going. If your monthly merchant statement looks like a wall of confusing codes and shifting percentages, that's often by design. To understand how to lower merchant fees, you must move past the noise and focus on one specific number: the Effective Rate. This single metric cuts through the jargon and reveals exactly what you're paying for every dollar you process. If you aren't tracking this monthly, you're essentially flying blind while your processor controls the controls.

Calculating Your Effective Rate

The Effective Rate is the only metric that truly matters because it accounts for every cent that leaves your bank account, including interchange, assessments, and markups. To find yours, use this simple formula: (Total Fees / Total Sales Volume) x 100. For example, if you paid $1,250 in total fees on $50,000 of volume, your effective rate is 2.5%.

In 2026, benchmarks have shifted. A "good" rate for a retail business using physical hardware typically falls between 1.8% and 2.4%. If you're in professional services or e-commerce, you might see rates between 2.6% and 3.2% due to the higher risk of card-not-present transactions. If your rate is consistently higher than these ranges, you're likely paying for hidden inefficiencies. We recommend using our 2026 Merchant Audit Checklist to perform a line-by-line review and see where your margins are leaking.

Spotting Disguised Markups

Once you've calculated your rate, it's time to hunt for "Junk Fees." These are administrative charges that provide zero operational value. Watch for these common warning signs on your next statement:

- PCI Non-Compliance Fees: This is often a monthly penalty ranging from $20 to $100. It should disappear the moment you complete your annual security profile.

- IRS Reporting Fees: Some processors now charge a "service fee" just to provide the 1099-K form that they're legally required to send you anyway.

- Non-Qualified Surcharges: If you see transactions labeled as "Non-Qual," it means your processor has moved them into a higher-cost tier. This usually happens because the data provided was insufficient or your pricing model is outdated.

You should also perform an "Inconsistency Audit." If your rates fluctuate during months when Visa and Mastercard haven't announced official updates, your processor might be quietly increasing their own margin. You shouldn't have to pay a premium for basic service. For instance, next-day deposits should be a standard expectation for your liquidity, not a paid add-on. If your current statement is full of these red flags, it's a great time to request a transparent review of your processing to ensure you're keeping more of what you earn.

Strategic Payment Routing: Moving Beyond High-Cost Credit Cards

Once you've audited your statements and identified the hidden leaks, the next step in your journey to financial efficiency is active routing. Think of every transaction as a choice. If you treat a $50 retail swipe the same way you treat a $5,000 corporate invoice, you're leaving money on the table. Learning how to lower merchant fees effectively requires a "concierge" approach to your payment methods. By steering specific transactions toward lower-cost paths, you protect your margins without sacrificing the customer experience. This isn't about restricting how people pay; it's about optimizing the backend data to ensure you aren't overpaying for the privilege of getting paid.

Strategic routing is a core pillar of managed care for your business operations. It moves you away from a passive "accept all" mindset and toward a proactive strategy where your payment infrastructure works for you. When you align the right payment method with the right transaction size, the savings accumulate quickly. This is where professional-grade tools and industry expertise become your greatest defenders against unnecessary costs.

Level 2 and Level 3 Data Optimization

If your business frequently accepts corporate, business, or government cards, you're likely paying some of the highest interchange rates in the industry. However, the card networks offer a significant discount if you provide more detailed transaction data. This is known as Level 2 and Level 3 processing. By including information such as tax IDs, invoice numbers, and freight codes, you reduce the perceived risk of the transaction. In exchange, Visa and Mastercard lower the interchange rate.

The ROI of this automated data is substantial. Many businesses see a reduction of up to 1% on their corporate card transactions simply by providing this extra layer of transparency. Modern, integrated POS systems can automate this data entry, ensuring you qualify for the lowest possible rates without adding extra work for your staff. It's a simple "if-then" scenario: if you provide the data, then you keep more of your revenue.

The Power of ACH for High-Ticket Invoices

For large transactions, credit cards are often the most expensive way to move money. Consider a $5,000 invoice. At a standard 2.9% rate, that single transaction costs you $145 in fees. An ACH (Automated Clearing House) transfer, by contrast, typically costs a small, flat fee that is a fraction of that amount. This makes ACH the ultimate "fee killer" for high-ticket service providers and B2B wholesalers. It's one of the most direct ways to understand how to lower merchant fees on a massive scale.

Some owners worry that customers will resist moving away from cards, but current B2B trends show the opposite. Most professional clients prefer the security and simplicity of bank transfers over managing credit limits or mailing physical checks. When you integrate ACH directly into your QuickBooks workflow, reconciliation becomes seamless and automatic. With next-day ACH deposits now widely available, the old "slow bank" objection has vanished, allowing you to maintain high liquidity while slashing your processing overhead.

Operational 'Quick Wins' to Slash Processing Costs Immediately

While auditing your statements and routing high-ticket invoices are essential long-term strategies, your daily operational habits also dictate your bottom line. Every time you process a payment, you're making a micro-decision that affects your effective rate. If your staff is manually keying in numbers instead of using a physical reader, or if your batches aren't settling on time, you're essentially choosing to pay more than necessary. Discovering how to lower merchant fees often comes down to these small, repeatable wins that protect your margins without requiring a complete overhaul of your business model.

Reducing Risk and Chargebacks

Processors view every transaction through the lens of risk. High risk translates to high fees. By implementing modern security protocols like EMV chip technology and 3D Secure for online payments, you shift the liability for fraudulent transactions away from your business and back to the card issuer. This proactive stance does more than just stop theft; it keeps your risk profile low, which gives you leverage to negotiate better rates over time. Professional bookkeeping services also play a vital role here by helping you identify and fight fraudulent chargebacks with accurate, organized records.

PCI compliance is a set of security standards that, when met, eliminates the monthly non-compliance penalties that processors often use to pad their margins.

Hardware and Entry Methods

The way you enter a card's information is one of the biggest factors in determining the interchange cost. Physical hardware is almost always cheaper than a virtual terminal. When a card is "swiped" or "dipped" at a point of sale, the network has physical proof the card was present, which lowers the risk of fraud. Keyed-in entries, by contrast, are flagged as higher risk and hit with significantly higher fees. Even if you use mobile credit card processing, you must use encrypted, Bluetooth-connected readers to qualify for the best possible rates. Integrated POS hardware further reduces costs by eliminating manual entry errors that often trigger expensive "non-qualified" downgrades.

You should also pay close attention to your batching schedule. If you don't settle your daily transactions within 24 hours, the card networks may downgrade those transactions to a higher-cost tier. Setting your hardware to auto-batch every evening ensures you never miss a settlement window. Finally, the 2026 settlement has provided more flexibility regarding surcharging and cash discounts. If your margins are tight, you can now legally pass a portion of the processing costs to the consumer or offer a discount for lower-cost payment methods like debit. If you are ready to upgrade your hardware and stop overpaying for keyed-in transactions, explore our integrated POS solutions today.

Beyond the Percentage: Why Your Processor Should Be Your Advocate

Lowering your costs isn't just a math problem; it's a partnership strategy. While many providers focus solely on the transaction, we believe your processor should be a defender of your time and resources. If you're constantly fighting with your statement, you aren't just losing money; you're losing the focus required to grow your business. Moving toward a 'Managed Care' model means your financial workflow finally stops working against you. By integrating your processing with your payroll and bookkeeping, you create a closed-loop system that identifies inefficiencies before they become expensive habits. This holistic approach is the true answer to how to lower merchant fees in a way that actually sticks.

Liquidity is often the 'hidden profit' that business owners overlook. If your funds are sitting in a processor's account for three days, you're essentially giving them an interest-free loan while your own cash flow suffers. We treat next-day deposits as a standard requirement for operational health, not a premium feature. When you have faster access to your funds, you can negotiate better terms with your own suppliers and avoid the costs associated with short-term credit. It's a simple logic: if you have the cash, then you have the control.

The Efficiency Dividend

Consider the hours your team spends on manual reconciliation. Every time a transaction is manually entered into QuickBooks or Xero, you risk a human error that could take hours of bookkeeping to untangle. The 'True Cost' of a cheap processor often hides in these administrative black holes. When your payments auto-sync with your accounting software, you gain an immediate efficiency dividend. You aren't just saving on the rate; you're reclaiming hours of high-value time. This transition from a vendor relationship to a strategic ally relationship is what allows you to focus on your craft while we handle the administrative managed care.

Next Steps: Your Path to Lower Fees

Your journey to a better bottom line begins with clarity. We offer a transparent LyrxPay Audit to analyze your current statements and find immediate opportunities for savings. We don't hide behind jargon or complex tiered models. Instead, we present a structured path forward that prioritizes your liquidity and operational ease. Our goal is to move you from a state of curiosity to a state of total confidence in your financial operations. If you're ready to see the difference a dedicated advocate can make, request a transparent fee analysis and see the LyrxPay difference today. You've done the hard work of building your business; let us do the heavy lifting of protecting your revenue.

Take Control of Your Financial Future

You've seen that the path to higher margins isn't just about finding a lower percentage; it's about a managed care approach to your entire financial workflow. By mastering your effective rate and implementing strategic routing for high-ticket invoices, you move from a state of frustration to a state of operational confidence. You now have the specific tools to identify "fee creep" and the knowledge to demand total transparency from your providers. Understanding how to lower merchant fees is the first step toward reclaiming thousands in lost revenue.

The real value comes from a partnership that prioritizes your liquidity through next-day deposits and eliminates administrative friction with seamless QuickBooks and Xero integration. You deserve a transparent, interchange-plus pricing model that protects your resources rather than draining them. We're here to act as your advocate, ensuring your payment infrastructure supports your growth instead of hindering it.

Stop overpaying and start growing with LyrxPay’s low-fee processing solutions. You've built your business with dedication and hard work. Now, let us help you keep more of what you earn so you can focus on your next phase of success.

Frequently Asked Questions

What is a typical merchant fee for a small business in 2026?

A typical effective merchant fee in 2026 generally ranges between 2.20% and 2.35% for most small businesses. This average reflects the 10-basis-point reduction following the 2026 Visa-Mastercard settlement. If your effective rate is significantly higher than this range, it's a clear indicator that your processor might be layering on unnecessary markups or that your current entry methods are inefficient.

Can I really negotiate my credit card processing rates?

You can absolutely negotiate the processor's markup portion of your credit card processing rates. While the wholesale interchange rates set by Visa and Mastercard are non-negotiable, the service fee charged by your provider is flexible. Businesses with consistent transaction volume or low chargeback rates have the most leverage to secure better terms during a professional contract review.

What are 'junk fees' and how do I get them removed from my statement?

Junk fees are arbitrary administrative charges like statement fees, IRS reporting fees, and PCI non-compliance penalties that provide zero operational value. To get them removed, you must first identify them through a line-by-line audit and then present these findings to your provider. If they refuse to eliminate these nuisance costs, it's often a signal that you need a more transparent and supportive partner.

How does Level 3 processing lower my B2B transaction costs?

Level 3 processing lowers your B2B costs by providing extra transaction data that qualifies you for discounted interchange rates from the card networks. By including line-item details like product codes and tax amounts, you reduce the perceived risk of the transaction. This is one of the most effective strategies for how to lower merchant fees when dealing with corporate or government cards.

Is ACH processing safer and cheaper than credit cards for my business?

ACH processing is significantly cheaper than credit cards because it utilizes a low, flat fee rather than a percentage of the total transaction. For a high-ticket invoice, an ACH transfer costs a fraction of what a credit card swipe would. It's also highly secure, as it moves funds directly between bank accounts, which drastically reduces the risk of chargebacks and card-related fraud.

How long does it take to switch to a lower-fee merchant service provider?

Switching to a lower-fee provider typically takes between three to seven business days from the initial application to full implementation. This timeline includes the underwriting process and the configuration of your new point-of-sale hardware. A professional ally handles the heavy lifting during this transition, ensuring your daily operations and cash flow remain completely uninterrupted.

Does QuickBooks integration help lower my overall merchant costs?

QuickBooks integration helps lower your overall merchant costs by eliminating the expensive labor hours associated with manual data entry and reconciliation. When payments auto-sync with your accounting software, you remove the risk of human error and gain an immediate efficiency dividend. This streamlined workflow is a critical component of how to lower merchant fees through proactive operational management.

What is the difference between interchange-plus and tiered pricing?

Interchange-plus is a transparent model where you pay the actual wholesale cost plus a fixed, disclosed markup. Tiered pricing, by contrast, bundles transactions into arbitrary buckets like "qualified" or "non-qualified," which often hides the true cost of processing. Interchange-plus is almost always the more cost-effective choice because it prevents processors from pocketing the spread on low-cost debit transactions.