Merchant Account for Service Businesses: The 2026 Guide to Payment Strategy

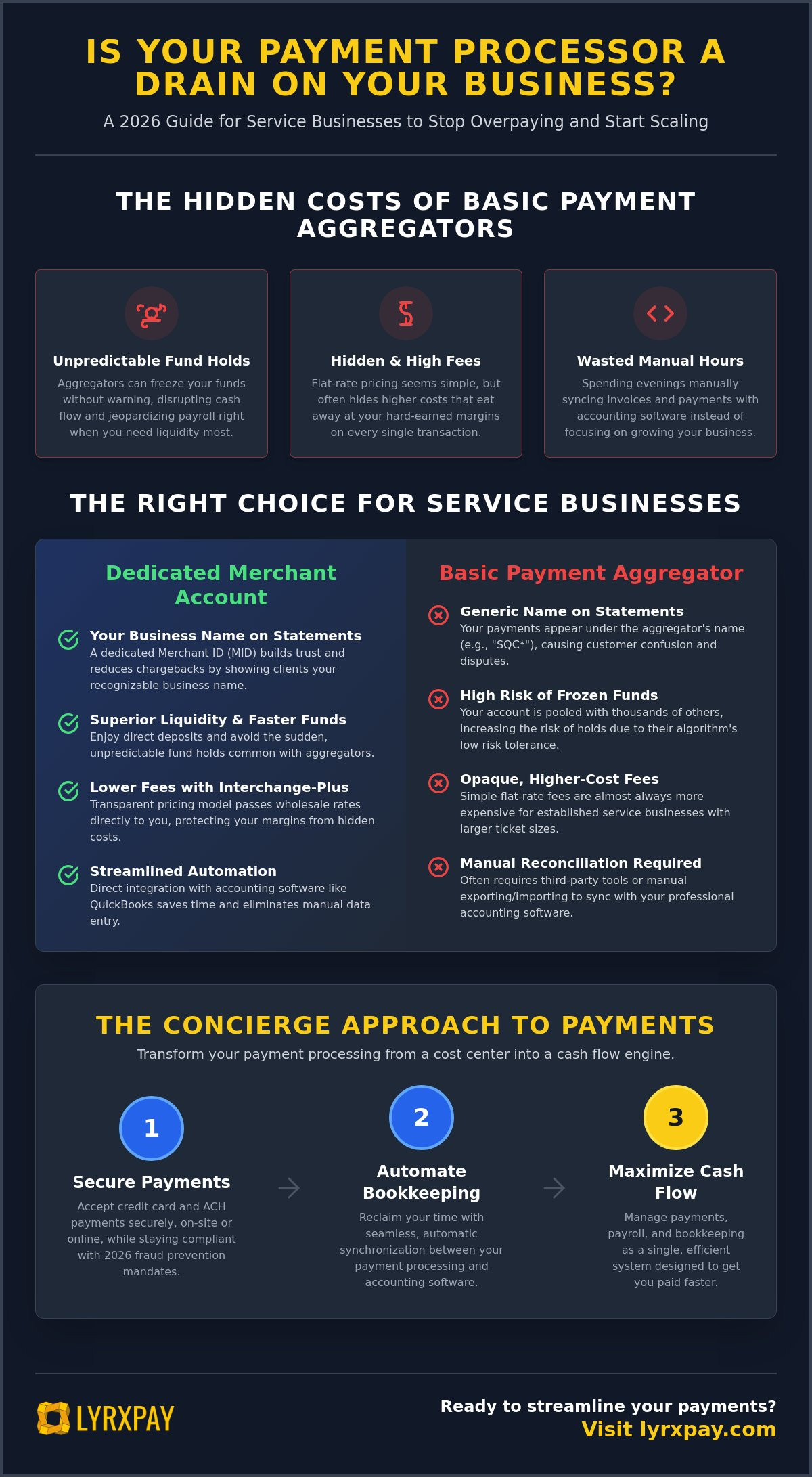

Relying on a basic payment aggregator isn't just a convenience; it's a quiet drain on your service business's liquidity. You've likely felt the sting of a sudden fund hold right when you needed to cover payroll, or watched high transaction fees chip away at your hard-earned margins. Choosing the right merchant account for service businesses is the difference between struggling with cash flow and scaling with confidence.

We believe you deserve a payment strategy that works as hard as you do. It's frustrating to spend your evenings manually syncing invoices with your accounting software when you should be focusing on your craft. This 2026 guide will show you how to transform your processing from a cost center into a streamlined cash flow engine. We'll preview how to secure faster access to your funds, navigate the new 2026 ACH fraud prevention mandates, and leverage automated bookkeeping to reclaim your time. It's time to stop overpaying for the simple act of getting paid.

Key Takeaways

- Learn how a dedicated Merchant ID builds professional trust and ensures your business name appears clearly on client bank statements.

- Discover why a dedicated merchant account for service businesses offers superior liquidity compared to standard payment apps that often trigger unpredictable fund holds.

- Identify the specific "Interchange-Plus" pricing models that lower your transaction fees and protect your service margins from hidden costs.

- Find out how to reclaim your time by automating the sync between your payment processing and accounting software like QuickBooks.

- Explore the concierge strategy for managing payments, payroll, and bookkeeping as a single, efficient system to maximize your cash flow.

What is a Merchant Account for Service Businesses?

Think of your merchant account as the essential bridge between your client's wallet and your business bank account. To understand What is a Merchant Account in a professional context, you have to look beyond a simple holding tank for money. It's a specialized financial arrangement that allows you to accept credit cards, debit cards, and ACH transfers. Unlike a standard checking account, this setup is designed specifically to handle the complexities of electronic payment settlements and fraud protection.

For a professional provider, the Merchant ID (MID) is your digital fingerprint. When you use a dedicated merchant account for service businesses, your actual business name appears clearly on the client's bank statement. This small detail reduces "friendly fraud" and chargebacks that happen when a client doesn't recognize a generic payment aggregator's name on their bill. It's about establishing a professional presence from the first quote to the final receipt.

Your service business requires a strategy that handles both "on-the-spot" field payments and complex "invoice-based" billing cycles. Retail accounts aren't built for the 30-day or 60-day cycles common in professional services. For firms managing ongoing retainers, utilizing tools from Churn Solution can help automate retention and prevent revenue loss from failed payments. Because your margins depend on the total cost of doing business, your account should offer a fee structure that respects your specific industry rather than treating you like a high-volume convenience store.

Service vs. Retail: Why Your Account Needs Differ

Retail stores thrive on high-volume, low-dollar transactions. Your service business likely operates on the opposite end of the spectrum. Whether you're an HVAC contractor, a legal consultant, or a medical provider, your average ticket size is significantly higher. This higher value means a single disputed transaction can hurt your cash flow much more than a retail shop losing a twenty-dollar sale.

You also need flexibility that a fixed retail terminal can't provide. Field contractors need mobile payment solutions that work on-site, while consultants might rely heavily on Card-Not-Present security for remote billing. A merchant account for service businesses must balance this need for mobility with robust security protocols to protect these larger payments.

Key Terminology for the Modern Service Provider

Understanding the components of your financial stack helps you spot where you might be losing money. These terms define the path your money takes:

- Payment Gateway: This is your digital storefront. It's the software that encrypts sensitive data and sends it to the processor, whether you're swiping a card in the field or sending a digital invoice.

- Acquiring Bank: This is the financial institution that maintains your merchant account and accepts the deposits from the card-issuing banks on your behalf.

- Merchant Services: This is the total ecosystem. It includes your processing, the hardware you use, and the software integrations that link your payments to your bookkeeping.

How Professional Payment Processing Works

When your client taps their phone on your terminal or pays a digital invoice, a complex chain of events triggers instantly. Within roughly three seconds, a signal travels from the payment interface to the card network, hits the client's bank for approval, and returns a response. While this speed is impressive, the real value of a professional merchant account for service businesses lies in what happens behind the scenes to ensure that "Approved" message actually turns into available cash.

Your processor acts as a vigilant guardian during this journey. They don't just move data; they verify that the funds exist and employ sophisticated tools to prevent fraud. This is especially critical in 2026, as the ACH Network has implemented stricter rules requiring participants to use more robust, documented processes for identifying fraudulent transactions. If you're looking for a partner to manage these complexities, choosing a provider that offers integrated credit card and ACH processing ensures your business stays compliant with these evolving standards without extra manual effort.

The Life Cycle of a Service Transaction

Understanding the path of your money helps you manage your business liquidity more effectively. The process follows three distinct stages:

- Authorization: The system checks if the client has sufficient credit or funds. For a service provider, this is your first line of defense against non-payment.

- Capture: This occurs when you finalize the transaction. In a retail setting, this happens at the point of sale; for service pros, it often happens when you "batch out" at the end of the day after the work is complete.

- Settlement: This is the final move. The funds are transferred from the card-issuing bank to your merchant account, eventually landing in your business bank account.

Understanding the Underwriting Process

Why does a professional account require an application while a basic app lets you start in minutes? The answer is stability. Professional accounts go through "upfront underwriting," where the processor evaluates your business history, service type, and expected volume. While this requires more effort initially, it prevents the "sudden freeze" many businesses experience with aggregators.

By verifying your business upfront, the processor establishes a baseline for your typical transaction size. This is vital for service providers who often have higher ticket prices that might otherwise trigger fraud alerts. To prepare for this process, you'll generally need your Tax ID (EIN), recent business bank statements, and copies of any required professional licenses. This transparency creates a foundation of trust, ensuring your access to funds remains uninterrupted even as your business grows.

Merchant Accounts vs. Payment Aggregators: The Liquidity Debate

Many service providers start their journey with payment aggregators like Square or Stripe because the signup process takes minutes. It feels like the path of least resistance. However, for a growing company, this "easy" start often leads to a restrictive ceiling on cash flow. Choosing a dedicated merchant account for service businesses represents a shift from being a guest in a shared pool to having a private, secure lane for your revenue.

The fundamental difference lies in ownership. In an aggregator model, you don't have your own Merchant ID; you're simply a sub-merchant under their massive umbrella. While this allows for instant access, it also means the provider has to manage enormous risk across millions of users. They use aggressive algorithms to spot trouble, and unfortunately, the normal billing patterns of a professional service business often look like "trouble" to a computer.

Why Aggregators Might Hold Your Service Revenue

The "Aggregator Trap" usually snaps shut when you process a transaction that deviates from a tiny retail average. If you're a contractor who suddenly swipes a $5,000 deposit for a new project, an aggregator's automated system might flag this as a "high ticket" red flag and freeze the funds for weeks. They do this because they haven't performed the deep underwriting we discussed previously. They're protecting themselves, not you.

Risk pooling is another hidden danger. In a shared environment, your account stability is partially tied to the behavior of every other business in the pool. If the aggregator sees a spike in fraud within your general industry category, they may tighten restrictions on everyone, including you. Having a direct, professional relationship with your provider ensures that your specific business history is the only metric that matters.

Maximizing Cash Flow with Next-Day Deposits

For a service business, liquidity is the lifeblood of operations. You need to pay your crew, purchase materials, and cover overhead without waiting for a third-party app to release your earnings. Understanding the mechanics of Understanding Merchant Settlement Timelines is essential for any owner looking to optimize their back office.

Dedicated accounts often offer next-day funding options that aggregators struggle to match. Imagine the strategic advantage of having your Friday service revenue cleared and available in your bank by Monday morning. This speed allows you to reinvest in your business immediately rather than hovering over a dashboard waiting for a transfer. Faster access to funds means you can take on larger projects with confidence, knowing your cash flow can support the upfront costs of professional service delivery.

Choosing the Right Merchant Service Provider in 2026

Selecting a partner for your financial infrastructure is a decision that dictates your operational speed for years to come. In 2026, the standard for a merchant account for service businesses has shifted away from mere "card acceptance" toward total financial integration. You need a provider that doesn't just process transactions but actively protects your margins through transparent pricing and smart data handling. Don't settle for a provider that treats your professional firm like a generic retail storefront.

Prioritizing "Interchange-Plus" pricing is the most effective way to lower your overhead. While flat-rate models might seem simpler, they often hide the true cost of processing by charging you a high, fixed percentage regardless of the card type used. With Interchange-Plus, you pay the actual wholesale cost set by the card networks plus a small, transparent markup. This ensures you benefit from lower rates on debit cards and basic credit cards, rather than paying a premium on every single swipe.

If your service business works with other companies, Level 2 and Level 3 data processing is non-negotiable. These protocols allow you to pass additional information, such as invoice numbers and tax codes, through the payment gateway. In exchange for this extra data, card networks often grant significantly lower interchange rates on B2B and corporate cards. It's a simple way to reclaim a percentage of your revenue on every large-scale contract you sign.

The Technical Checklist: Software and Hardware

Your field operations require tools that bridge the gap between the job site and the office. Before signing a contract, verify that the provider's mobile POS hardware is rugged enough for on-site technicians and integrates seamlessly with your mobile devices. You should also ensure the system can handle recurring billing for maintenance contracts or retainer agreements automatically. For a detailed look at how different providers stack up this year, consult our guide on the Best Payment Processor for Small Business.

Fee Transparency: Avoiding the 'Hidden' Cost

The most frustrating part of merchant services is discovering "junk fees" on your monthly statement. Look out for line items like statement fees, annual fees, or PCI non-compliance penalties that can quietly erode your profits. A professional partner will help you maintain compliance rather than charging you for failing to meet it. Furthermore, next-day deposits should be a standard expectation for any modern merchant account for service businesses, not a luxury add-on that carries an extra fee. If you're tired of guessing what your actual costs will be, you can request a transparent rate review to see exactly where your money is going.

Your back office deserves a rest from manual data entry. Evaluate the quality of QuickBooks and Xero integrations before making a final choice. A high-quality integration doesn't just "import" data; it maps payments to specific invoices and reconciles your bank accounts in real time. This automation eliminates human error and ensures your bookkeeping is always audit-ready, allowing you to focus on delivering exceptional service to your clients.

If you are looking for dedicated support in managing your back office, Thank Heavens Bookkeeping offers professional bookkeeping services designed to keep your financial records accurate and audit-ready.

LyrxPay: The Concierge Approach to Service Payments

LyrxPay operates as a dedicated advocate for your time and resources. We recognize that a merchant account for service businesses shouldn't be a source of stress or a drain on your margins. Instead, it should be a silent, efficient engine that powers your growth. Our "concierge" model moves away from the cold, clinical feel of traditional financial services. We offer a high level of personal attention that ensures your specific operational needs are met without the typical industry jargon or hidden complexity.

The true strength of our approach lies in the synergy between our core offerings. By integrating your credit card and ACH processing with our payroll solutions and bookkeeping services, we create a unified financial stack. This "all-in-one" ecosystem eliminates the gaps where errors usually occur. When your payments, your staff's wages, and your ledger all speak the same language, you gain a level of clarity that most service providers never achieve. We focus on cutting through the technical noise to deliver a streamlined experience that protects your bottom line.

Liquidity remains our top priority for your business health. We understand that waiting for funds can stall a project or delay a necessary purchase. That's why we emphasize the "Next-Day Deposit" advantage as a standard expectation. You've done the work; you should have access to the revenue. This commitment to fast funding ensures that your cash flow remains consistent, allowing you to focus on your craft rather than your bank balance.

Seamless QuickBooks Integration

Manual data entry is a relic of the past that still haunts many modern offices. LyrxPay eliminates this burden through an expert sync with QuickBooks and Xero. Our system doesn't just dump data into your software; it maps every transaction to the correct invoice and reconciles your accounts automatically. This gives you real-time visibility into your financial health. You'll always have a single point of contact for both your payments and your bookkeeping, ensuring that any questions are resolved by someone who actually understands your entire business flow.

Ready to Optimize Your Service Revenue?

It's time to move from a transactional mindset to a strategic one. Your payment processing should be a tool for scale, not a hurdle to overcome. By choosing a partner that prioritizes transparency and advocacy, you reclaim the hours spent on administrative tasks and the dollars lost to inefficient fee structures. Experience a higher level of managed care for your back office and see the difference that a dedicated partner makes in your daily operations.

Explore LyrxPay's Service Business Solutions

Secure Your Service Margins for 2026

You've spent years building your reputation; don't let an outdated payment strategy hold you back. Transitioning to a dedicated merchant account for service businesses is about more than just taking cards. It's about securing your liquidity and ensuring your hard-earned revenue is available when you need it most. By choosing interchange-plus pricing over flat-rate models, you effectively cut through industry jargon to keep more of your profit.

When you automate your bookkeeping with seamless QuickBooks or Xero sync, you reclaim the hours lost to manual entry. This shift from a transactional relationship to a strategic partnership allows you to focus on your craft while we manage the administrative weight. Ready to experience a concierge approach to your finances? Upgrade to a Professional Merchant Account with LyrxPay to benefit from next-day deposits and a partner who advocates for your growth. You focus on delivering exceptional service. We'll handle the complexities of getting you paid.

Frequently Asked Questions

Is a merchant account different from a business bank account?

Yes, a merchant account is a specialized financial arrangement, not a replacement for your standard business bank account. While your checking account holds your operating capital, the merchant account acts as a secure transit point for electronic payments. It handles the complex communication between card networks and banks to ensure funds are verified and settled correctly before they land in your business account.

How long does it take to get approved for a merchant account?

Approval for a professional merchant account typically takes between 24 and 48 hours. While some apps offer instant setup, they often skip the critical underwriting process required for long-term stability. This upfront verification for a merchant account for service businesses ensures your account remains active. It prevents the sudden fund holds common with "instant" models by establishing your business legitimacy from day one.

Why are my service business's transaction fees so high?

High fees usually stem from flat-rate pricing models that charge a high, fixed percentage regardless of the card type used. Service businesses often process Card-Not-Present transactions or high-value invoices, which carry higher inherent risk. Switching to an interchange-plus model allows you to pay the actual wholesale cost of the transaction plus a small, transparent markup, which often lowers your total monthly expenses.

Can I accept ACH payments through a merchant account?

Yes, you can accept ACH payments through a professional merchant service setup. ACH transfers are often the most cost-effective way to handle large service invoices because they carry much lower fees than credit cards. In 2026, these transactions are subject to stricter fraud prevention rules, making a professional provider's guidance essential for staying compliant with the latest Nacha network requirements.

What happens if a client disputes a service charge (chargeback)?

If a client disputes a charge, the processor initiates a chargeback investigation and temporarily removes the funds from your account. You'll need to provide evidence like signed service contracts, photos of completed work, or email correspondence to prove the service was rendered. Having a dedicated account gives you a professional advocate to help navigate the dispute process and protect your revenue from unfair claims.

Do I need special hardware to take payments on a job site?

You need mobile point-of-sale (mPOS) hardware designed for field work to accept payments on a job site. This usually includes a Bluetooth-connected card reader that syncs with your smartphone or tablet. These devices are built to handle the rigors of on-site service environments while ensuring every tap or swipe is encrypted and secure, providing a professional experience for your clients.

How does QuickBooks integration help my service business?

QuickBooks integration eliminates the need for manual data entry by automatically syncing your payment data with your accounting ledger. It maps payments directly to open invoices and reconciles your bank statements in real time. This automation saves your back office hours of administrative work and ensures your financial records are always accurate and ready for tax season without the stress of manual syncing.

What is the difference between flat-rate and interchange-plus pricing?

Flat-rate pricing charges one fixed percentage for every transaction, while interchange-plus pricing separates the wholesale cost from the provider's fee. Flat-rate models are simple but often more expensive because they must cover the cost of high-end rewards cards. Interchange-plus is more transparent and usually results in lower overall costs for a merchant account for service businesses, especially those with consistent or growing transaction volumes.